Recent events in Iran and the Middle East have overshadowed newly released data from the Bank of Italy regarding the country’s public debt at the end of last year and its composition by sector.

The data warrants attention as it highlights a significant acceleration since 2022 in the amount of Italian public debt held by two key groups: households and businesses, and foreign investors. Following successful government bond placements in recent years, Italian public debt held by families and businesses now totals €447 billion as of the end of 2025, representing 19.8% of Italy’s GDP. Debt held by non-resident investors has reached €1.064 trillion, equivalent to 47.1% of GDP. Simultaneously, holdings by banks, insurance companies, and the Bank of Italy have decreased.

A New Phase

Prior to the introduction of the Euro, Italian households and businesses played a dominant role as holders of the country’s public debt. However, their share subsequently declined, initially due to lower interest rates on Italian government bonds with the advent of the Euro, and later due to financial shocks from the Greek debt crisis. Now, with the turbulent period of the sovereign debt crisis behind it and renewed confidence in bonds from Southern European countries, the contribution of investors to the financing of Italian debt is becoming increasingly significant. According to Eurostat data, Italian families have shown a growing interest in government bonds since the post-Covid period, reinvesting a substantial portion of their financial wealth into public debt.

Italian public debt held by families, after reaching a low of 9% of GDP in 2021, rose to 10.5% in 2022, then to 14.6% in 2023 and 15.6% in 2024 (data for 2025 broken down between families and businesses is still pending). During the same period, debt held by domestic non-financial businesses remained relatively stable, representing 3.4% of GDP in 2024. Combined, these two groups (families and businesses) now hold public debt equivalent to 19% of GDP in 2024, with a further increase to 19.8% in 2025.

Reassured by political stability and prudent management of public finances, foreign investors have also returned to Italian government bonds with confidence. Italian public debt held by non-resident investors, after reaching a low of 36.5% of GDP in 2023, rose to 41.6% in 2024 and 47.1% in 2025. Compared to pre-Covid levels in 2019, debt held by families and businesses has increased by 7.1 percentage points of GDP over six years, while that held by non-resident investors has increased by 4.7 percentage points.

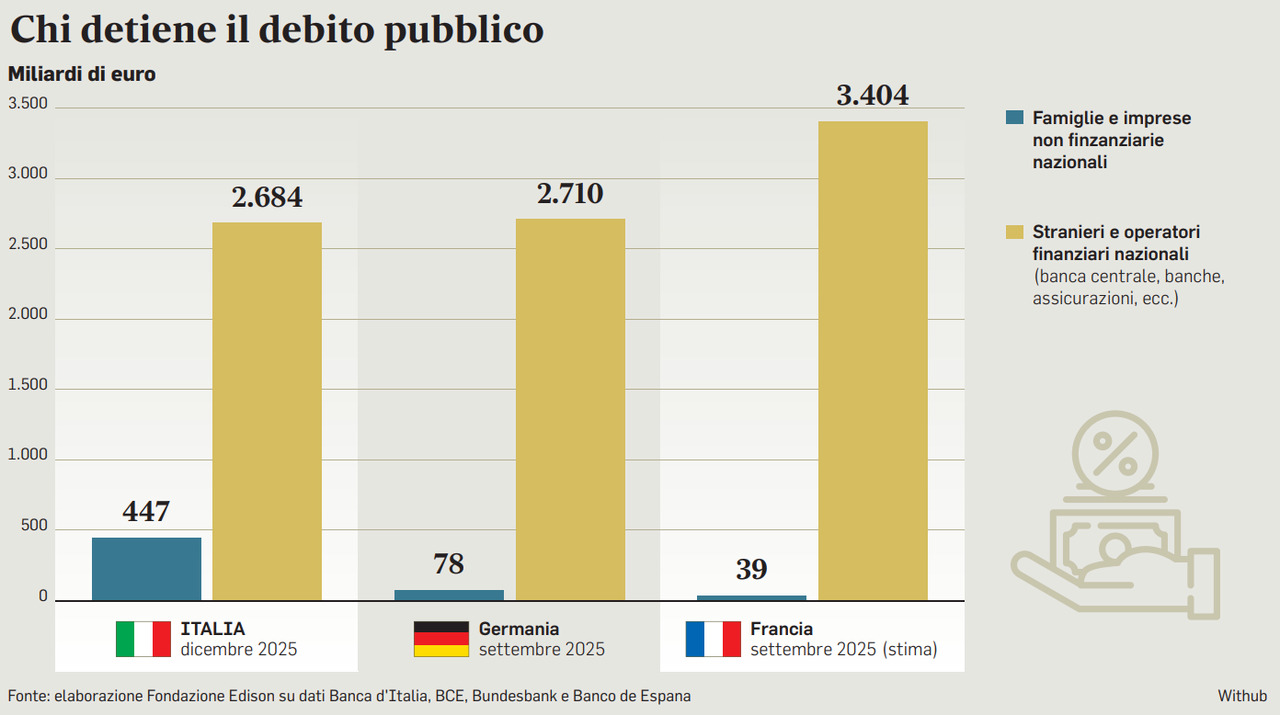

As of the end of 2025, the breakdown of Italian public debt was as follows: Bank of Italy 18.5%, banks 20.0%, insurance companies, funds, and other financial intermediaries 12.7%, families and businesses 14.4%, foreign investors 34.4%. Expressed as a percentage of GDP, the public debt held by families and businesses in Italy (19.8%) is the highest in the Eurozone. The share of non-financial private entities does not reach 1.5% in France or 2% in Germany. While the debt held by families and businesses in Italy is significantly higher than in France and Germany, the debt held by foreigners and domestic financial entities in Italy is lower in absolute value than the corresponding debts of France and Germany.

Sustainability

Italian public debt held by foreigners has grown by €332 billion between 2023 and 2025, thanks to renewed market confidence. However, even after this surge, it represents a relatively sustainable percentage of total debt, remaining below 35%. In Germany, this share is between 45% and 50%, while in France it is pushing beyond 55%. In absolute terms, while Italy’s foreign-held debt exceeded €1 trillion at the end of 2025, Germany’s had reached €1.416 trillion as of September of last year, and France’s, which was already at €1.754 billion at the end of 2024, could approach or even exceed €1.9 trillion at the end of 2025 (data not yet available). In effect, foreigners have financed a large part of the recent growth of the debt that underpins the French welfare state. And, now that France is no longer considered a “safe” country due to its exploding debt and the political inability to implement necessary reforms, foreign investors are demanding ever-higher rates to continue doing so.

Without the debt held by families and businesses—a significant “self-financing” component unique to Italy in Europe—the country’s debt-to-GDP ratio at the end of 2025 falls to 117.3%. As families and businesses in Italy hold only 1.3% of their country’s debt-to-GDP ratio, the public debts of Italy and France held by foreigners and domestic financial entities are now nearly equivalent as a percentage of GDP. This explains more than anything why the spread between France and Italy has narrowed to its lowest levels and even reversed in Italy’s favor in recent months.

© RIPRODUZIONE RISERVATA

© RIPRODUZIONE RISERVATA