The ongoing conflict involving the United States, Israel, and Iran is creating a “perfect storm” with potential repercussions for consumers and global supply chains, extending far beyond oil and gas prices. Each day the conflict continues restricts worldwide trade of goods—with impacts on the global economy that are significant, yet often overlooked. “The real vulnerability lies in derivatives, not crude oil,” according to a report by Felipe Elink Schuurman, co-founder of commodities trading firm Sparta, who warns that secondary effects impacting supply chains are already being felt and “this crisis goes far beyond the price of a barrel of oil.”

Prior to the crisis, five million barrels of petroleum derivatives passed through the Strait of Hormuz daily. The free flow of fertilizers, helium, fuel for ships and aircraft, aluminum, and distillates like naphtha has been disrupted. Steve Gordon, global research director at Clarksons, calculates in a report published on Monday that vessel traffic has decreased by 95% compared to pre-conflict levels. Just five vessels are now traversing the area on average, down from 125 just over two weeks ago. This disruption impacts 19% of all refined petroleum products consumed worldwide, according to data compiled by the United Nations Conference on Trade and Development (UNCTAD). It also affects 13% of all chemical products, including fertilizers, and 2% of dry grain.

India, China, Southeast Asian nations, and East Africa are the most affected by the supply shortages from the Middle East, whereas the United States is more insulated due to its own petrochemical industry. Europe faces rising costs but has less direct dependence on the conflict-affected countries. Experts at Barclays state that “the recent escalation of conflicts in the Middle East has profoundly underscored the fragility of global energy supply chains.”

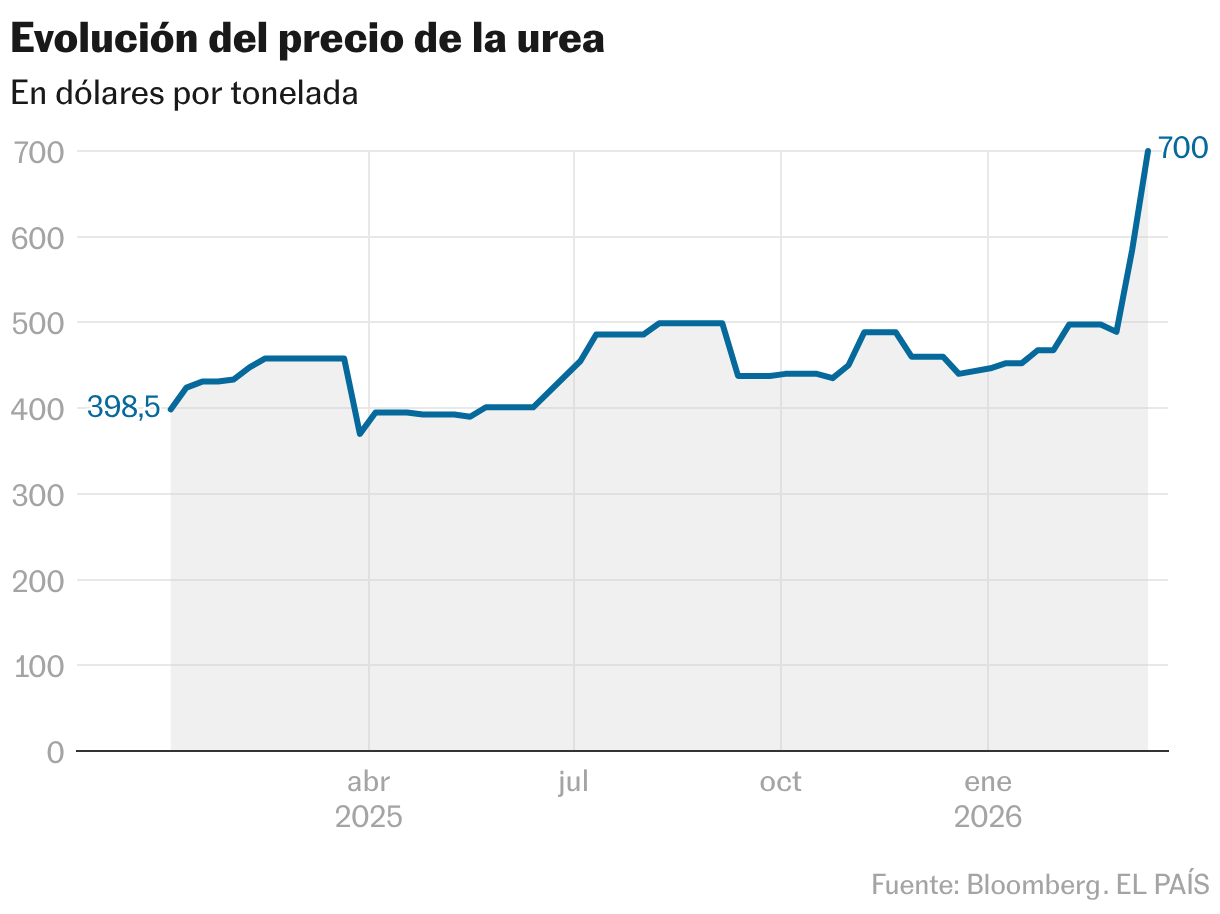

A third of all global fertilizer trade originates from countries in the Persian Gulf. This market was valued at 16 million tons in 2024, representing 67% of global urea consumption, 20% of diammonium phosphate (DAP), and 9% of monoammonium phosphate (MAP). These are all essential for the cultivation of crops like corn, rice, and wheat in countries such as Sudan, which imported 54% of its fertilizers from Gulf countries in 2024, and Australia (32%). Spain also relies on exports of nitrogenous and phosphate fertilizers from Saudi Arabia and Qatar for 7.4% of its needs, according to data from the Real Instituto Elcano. “The indirect implications for the global market could be drastic, and some regions could subsequently experience fertilizer shortages,” notes British consultancy CRU.

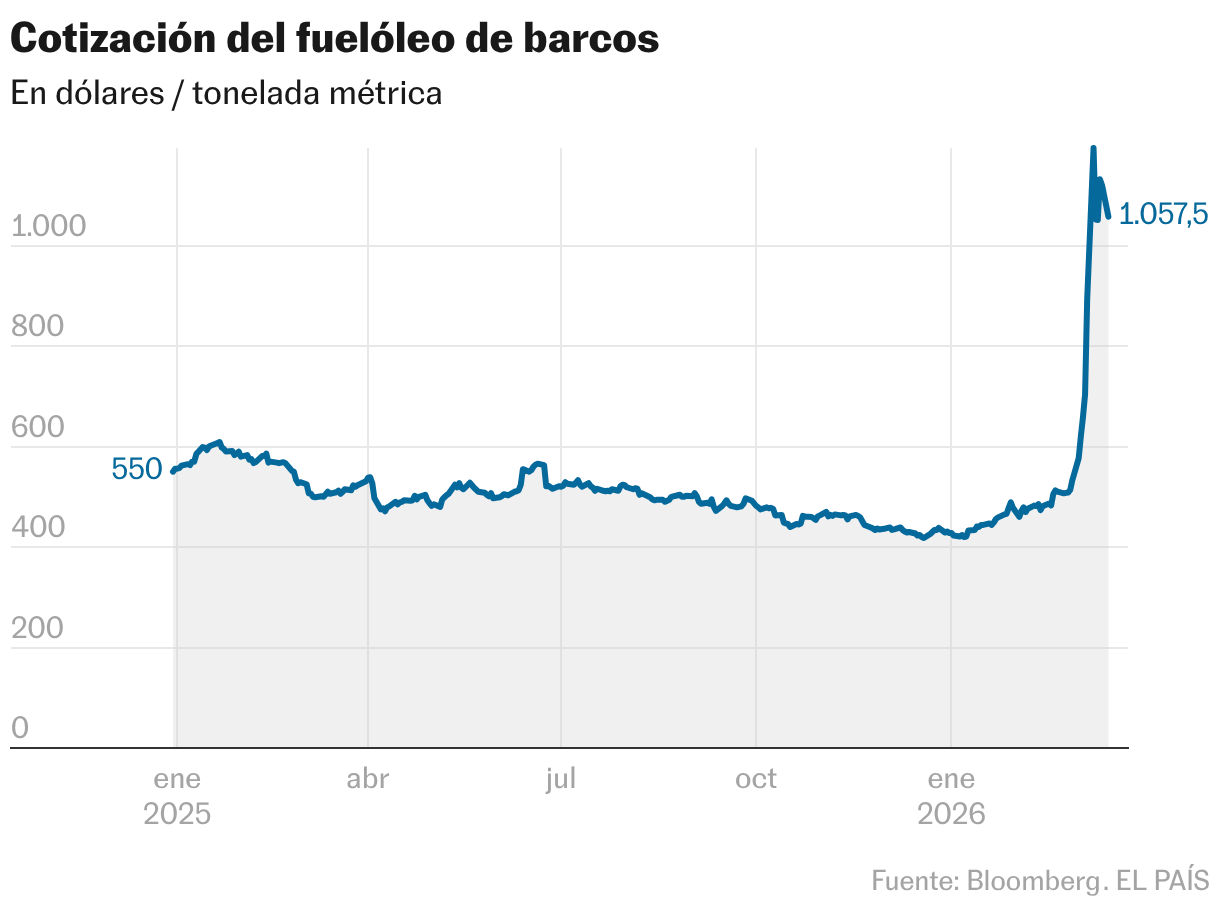

Beyond the 41% surge in the price of Brent crude, the benchmark for Europe, the conflict is impacting sharp increases in gasoline and diesel prices, as well as the cost of fuel for airplanes and ships. The International Air Transport Association (IATA) has warned of a potential increase in airfares of between 8% and 9%. The cost of ship fuel, light fuel oil, has climbed from $521.5 per ton to $1,119.5 in Singapore, the largest maritime fuel supply port. “Demand for marine fuel is structurally inelastic: ships cannot stop mid-ocean. If refineries are not operating, the supply of fuel oil is depleted once stocks are consumed,” Schuurman points out in his report.

Attacks by Iranian drones on energy facilities in Qatar forced state-owned QatarEnergy to halt production of liquefied natural gas and derivatives like naphtha, used by major Asian petrochemical companies to produce ethylene. This gas is an essential component in the production of plastics such as PVC, polyethylene, and polypropylene, used to manufacture packaging like plastic bottles, construction materials, and appliances. It is also crucial for steel foundries and the automotive industry in Southeast Asian countries. “Markets are not really considering the cascading implications of the naphtha supply shortage,” Mateen Chaudhry, founder and CEO of corporate advisory firm BCMG, told Bloomberg. “It could be the canary in the coal mine.”

Another consequence of the shutdown of Qatar’s Ras Laffan facilities is the significant decrease in global helium supply. Qatar is the world’s second-largest producer of helium, with 33% of global production, second only to the United States, according to data from the U.S. Geological Survey (USGS). While helium is commonly associated with inflating balloons, its uses are far more widespread. It is a key element in the technology industry, facilitating the manufacturing process of chips. This creates significant uncertainty for companies like TSMC, Samsung, and Intel, and, by extension, for tech giants like Nvidia, Microsoft, and Apple, which utilize these chips.

Analysts suggest that if the disruption to Qatar’s production extends for another 60 to 90 days, the cost of helium could surge by as much as 50%, given its limited shelf life of just 45 days before evaporation, hindering storage capacity. “A disruption in the Strait of Hormuz would not automatically halt chip production, but could have repercussions on energy costs, material supply, and the economics of building AI infrastructure,” Shawn Kim, head of technology research at Morgan Stanley, told Bloomberg.

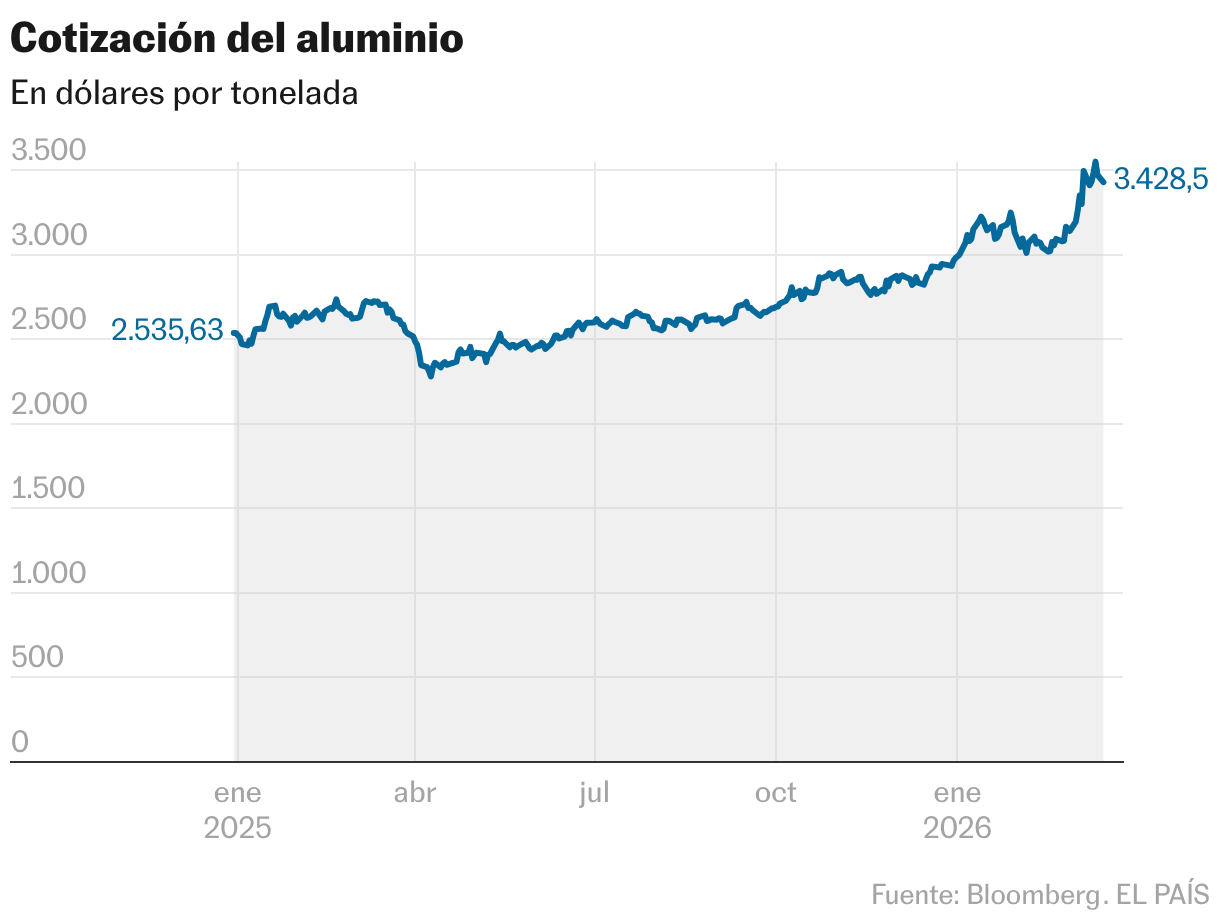

Rising prices are also being reflected in other industrial commodities, such as aluminum and coal. ING strategists believe aluminum could reach $4,000 per ton in a scenario of severe disruption “due to the concentration of export-oriented smelting capacity in the Gulf” and the existing market supply shortage. They note that countries in the Persian Gulf account for approximately 9% of global aluminum production. Coal, a fuel that could allow China to mitigate the rising costs of oil and natural gas, has risen 17.5% since the end of February.

The ramifications of the war initiated by the U.S. And Israel continue to emerge, even as U.S. President Donald Trump insists that Operation Epic Fury will soon conclude. Time will tell whether the second-round effects will be contained or extend and ultimately impact the price of the new iPhone or even a simple bottle of water.